Quick Links

- What Job Costing Tracks

- How This Is Different from Bookkeeping Or a P&L Report

- “Busy” and “Profitable” Aren’t the Same Thing

- A Quick Example: Estimated vs. Actual

- Where MyWorkbelt Fits In

Job costing is the practice of tracking exactly what a specific job costs you, broken down by labor, materials, and overhead, and comparing that to what you expected it would cost. It’s the difference between seeing overall annual profit and identifying individual job profitability

What Job Costing Tracks

Job costing breaks a single job into three buckets: labor, materials, and overhead.

Labor is the hours the job actually took, not the hours you quoted. Materials are what got pulled off the truck or ordered for that job specifically. Overhead is a slice of your fixed costs, like the truck payment or the office rent, allocated to that job, so the number reflects reality instead of just direct costs.

Put those three together, and you get one figure: what this job really cost you to run. Compare that to what you estimated when you quoted it, and you know whether the job made money.

Do that for every job, and patterns show up. Maybe every HVAC replacement runs long on labor. Maybe your commercial service calls are quietly subsidizing your residential work. You can’t see any of that from a bank balance.

How This Is Different from Bookkeeping Or a P&L Report

Your bookkeeper and your P&L report are looking at the whole business. Revenue in, expenses out, profit at the bottom. That number is real, and you need it, but it’s average.

Capterra’s own research on contractor accounting found the same setup at most small trade and construction businesses: one tool for estimating and scheduling, a separate tool for the books, and someone in the office manually moving numbers between the two every month. Job costing is what closes that gap, inside one system, instead of a manual bridge that only gets rebuilt once the invoices are already sent.

Job costing looks at one job at a time. It’s the difference between “the business made an 8% margin this quarter” and “this specific type of job is running at 3% while that other type is running at 15%, and the average is hiding both.”

A P&L also tends to arrive late. Monthly, quarterly, or at tax time, depending on your bookkeeper’s rhythm. By the time you see the number, the jobs that caused it are finished, the crew has moved on, and there’s no way to trace a soft margin back to the job type, the technician, or the supplier that caused it.

Job costing is built to answer a question your P&L was never designed to answer not “did we make money,” but “which jobs made money.”

“Busy” and “Profitable” Aren’t the Same Thing

Every trade business owner has had a month that looked great on paper and felt thin in the bank account. More jobs than usual, a full schedule, techs running all day. Then the number doesn’t match the effort.

You didn’t book bad jobs. That gap is almost always a job costing problem, not a sales problem. You booked jobs whose actual cost quietly ran past what you estimated, on materials, on labor, or on both, and nothing in your existing reporting was built to catch it while it was happening.

A busy calendar tells you demand exists. It says nothing about whether the jobs filling out that calendar are worth doing. Those are two different questions, and most trade businesses only have a system built to answer the first one.

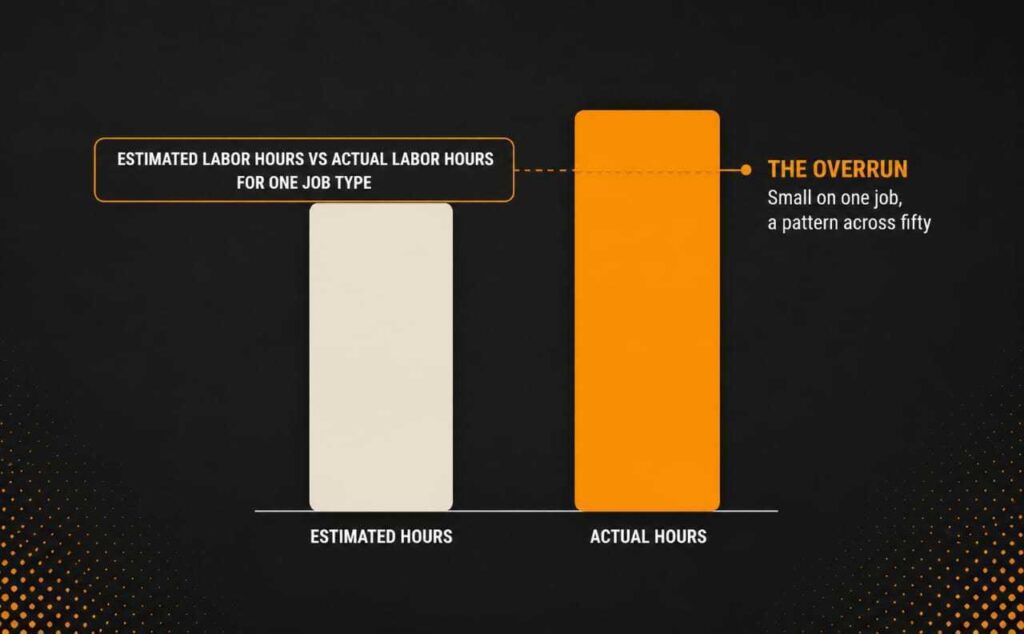

A Quick Example: Estimated vs. Actual

Here’s a simple, illustrative scenario. It isn’t tied to a real client or a specific dollar figure, just a pattern that plays out constantly in the trades.

Say a plumbing company quotes a common service call at a set of labor hours, based on how long that job type has always taken. On paper, every one of these jobs looks profitable, because the quote was built around that number.

Now say a specific fitting on newer installations takes longer to access and replace than the older version the estimate was written around. Each job runs a little over the estimated hours. Not enough to notice on any single invoice. The customer pays, the job closes, and everyone moves on.

Repeat that job type forty or fifty times a year, and that small overrun becomes a standing loss on an entire category of work. Nobody did anything wrong. The estimate just went stale, and nothing was tracking the actual hours against it closely enough to catch the drift.

That’s the entire value of job costing in one example. It’s not about catching a single bad job. It’s about seeing the pattern across many similar jobs before it becomes a permanent, invisible tax on that job type.

Where MyWorkbelt Fits In

Want to test this without buying anything? Pull your last ten closed jobs of one type. Write down what you quoted for labor and what the timesheets say actually happened. If gathering that takes more than an hour, that’s a finding too.

Most software shows you job costing data the way your accountant does: after the fact, once a quarter, or at tax time, when the jobs that caused the number are long gone. MyWorkbelt shows it to you in real time and reviews it with you every month in your Growth Review, with a named dedicated CSM who’s already looked at the numbers before you sit down.

Job costing was always the right question to ask. Most trade businesses just never had a system built to answer it before the year was already over.